Property Transfer Tax and Fee

Property transfer tax is a tax imposed on the registration of transfer of title to property from one person to another that apply to the transfer ownership of land, condominium or transfer land together with building or transfer only building). In Thailand, the property transfer tax and fee refers to 1. Transfer fee, 2. Specific business tax or stamp duty and 3. Withholding income tax.

1. TRANSFER FEE

Transfer fee is not a tax but a fee payable to the government service for registration of the transfer of the property. The transfer fee is fixed at the rate of 2% based on the appraised value of the property.

WHAT IS THE APPRAISED VALUE?

Appraised value is the value of the property (Land, Building and Condominium) based on the valuation established by the government (land department and treasury department) in order to fix the minimum price of the property for calculating transfer fee and tax.

WHAT IS THE APPRAISED VALUE?

Appraised value is the value of the property (Land, Building and Condominium) based on the valuation established by the government (land department and treasury department) in order to fix the minimum price of the property for calculating transfer fee and tax.

2. SPECIFIC BUSINESS TAX AND STAMP DUTY

Specific Business Tax is a tax applicable on property sale/transfer fixed at a rate of 3% on the higher value between the declared purchase price and the appraised value (Whichever is higher), plus a local tax of 10% on the specific business tax, bringing the total tax to 3.3%. The sale/transfer is not subject to the specific business tax if;

1. Selling property by an individual who has acquired the property for more than 5 years.

2. Selling property to the government under the expropriation law.

3. Selling inherited property.

4. Selling property by an individual who has his name recorded in the house registration book for not less than 1 year.

5. Transferring property as gift to a child but exclude adopted child.

6. Transferring property by inheritance to heirs.

7. Transferring property as gift to the government.

8. Exchange property with the government’s property.

Stamp Duty, in the transaction of property sale/transfer the stamp duty is charged only when the seller is not subject to the Specific Business tax at the rate of 0.5% on the higher value between the declared purchase price and the appraised value (Whichever is higher). In case Specific Business Tax is paid the transfer is exempt from the Stamp Duty.

1. Selling property by an individual who has acquired the property for more than 5 years.

2. Selling property to the government under the expropriation law.

3. Selling inherited property.

4. Selling property by an individual who has his name recorded in the house registration book for not less than 1 year.

5. Transferring property as gift to a child but exclude adopted child.

6. Transferring property by inheritance to heirs.

7. Transferring property as gift to the government.

8. Exchange property with the government’s property.

Stamp Duty, in the transaction of property sale/transfer the stamp duty is charged only when the seller is not subject to the Specific Business tax at the rate of 0.5% on the higher value between the declared purchase price and the appraised value (Whichever is higher). In case Specific Business Tax is paid the transfer is exempt from the Stamp Duty.

3. INCOME TAX (Corporate Income Withholding Tax and Personal Income Withholding Tax)

The income derived on the sale/transfer property in Thailand should be declared in Thailand. The land department has an authority to withhold the income tax immediately upon the registration of sale/transfer of property. The rates of income tax payable by individual and legal person is different. A legal person is taxed at a fixed rate of 1% on the declared purchase price or the appraised value of the property, whichever is higher, this withholding corporate income tax at 1% will be applicable only when the seller is a legal person (limited company or partnership and etc.). An individual (Natural Person) is taxed in accordance with 3 different calculation methods depending on the location of the property and the mode of acquisition of the property as follows;

3.1 Calculation of Personal Income Withholding Tax for property which is not inherited property and not property which is acquired by gift.

The tax can be calculated by stages as follows:

· Finding the appraised value of the property to be sold/transferred.

· Finding the holding year of the property (How long the seller has owned ownership of property counted from the year of receipt of ownership until the year of transfer, any fraction of a year shall be deemed a full year)

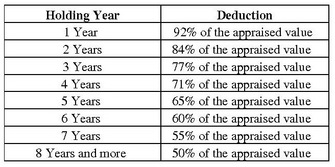

· Deduct/minus the appraised value with the deduction in accordance with the sliding scale as follows:

The tax can be calculated by stages as follows:

· Finding the appraised value of the property to be sold/transferred.

· Finding the holding year of the property (How long the seller has owned ownership of property counted from the year of receipt of ownership until the year of transfer, any fraction of a year shall be deemed a full year)

· Deduct/minus the appraised value with the deduction in accordance with the sliding scale as follows:

· After minus the appraised value with the deduction as mentioned above you will find a result, then divide such result by the holding year, after division you will have YEARLY INCOME.

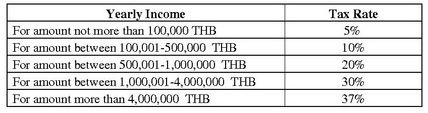

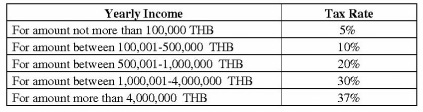

· Calculate YEARLY INCOME TAX by using YEARLY INCOME in accordance with the tax table as follows:

· Calculate YEARLY INCOME TAX by using YEARLY INCOME in accordance with the tax table as follows:

· After follow with above stage, you will have the YEARLY INCOME TAX, finally, the PERSONAL WITHHOLDING INCOME TAX shall be the amount of the YEARLY INCOME TAX multiply by HOLDING YEAR (YEARLY INCOME TAX times HOLDING YEAR is PERSONAL WITHHOLDING INCOME TAX)

SAMPLE CALCULATION FOR 3.1

· For example, the appraised value of the property is 4,000,000 THB

· At the transfer date, the seller has owned the property for 4 years and 2 months, so the holding year is 5 years.

· Minus the appraised value (4,000,000 THB) with the deduction (65% of 4,000,000 THB) = 4,000,000 – 2,600,000 = 1,400,000 THB.

· The result from above is 1,400,000 THB, then divide 1,400,000 by 5 (Holding Year), after the division, we have the YEARLY INCOME of 280,000 THB.

· Calculate YEARLY INCOME TAX by using YEARLY INCOME of 280,000 THB in accordance with the below tax table:

· At the transfer date, the seller has owned the property for 4 years and 2 months, so the holding year is 5 years.

· Minus the appraised value (4,000,000 THB) with the deduction (65% of 4,000,000 THB) = 4,000,000 – 2,600,000 = 1,400,000 THB.

· The result from above is 1,400,000 THB, then divide 1,400,000 by 5 (Holding Year), after the division, we have the YEARLY INCOME of 280,000 THB.

· Calculate YEARLY INCOME TAX by using YEARLY INCOME of 280,000 THB in accordance with the below tax table:

For the amount of 100,000 THB, yearly income tax is charged at rate of 5% or 5,000 THB.

For the amount of 180,000 THB, yearly income tax is charged at rate of 10% or 18,000 THB.

The total yearly income tax for yearly income of 280,000 THB is 5,000 + 18,000 = 23,000 THB

· As the final stage, the PERSONAL WITHHOLDING INCOME TAX shall be amount of 23,000 THB multiply by 5 (23,000 x 5 = 115,000 THB

· The personal withholding tax for the sample transaction is 115,000 THB

For the amount of 180,000 THB, yearly income tax is charged at rate of 10% or 18,000 THB.

The total yearly income tax for yearly income of 280,000 THB is 5,000 + 18,000 = 23,000 THB

· As the final stage, the PERSONAL WITHHOLDING INCOME TAX shall be amount of 23,000 THB multiply by 5 (23,000 x 5 = 115,000 THB

· The personal withholding tax for the sample transaction is 115,000 THB

3.2 Calculation of Personal Income Withholding Tax for inherited property and for property acquired by gift, in which, located in Bangkok, Pattaya, municipality and public health zone (a form of local government on a lower level than a municipality)

The tax can be calculated by stages as follows:

· Finding the appraised value of the property to be sold/transferred.

· Finding the holding year of the property (How long the seller has owned ownership of property counted from the year of receipt of ownership until the year of transfer, any fraction of a year shall be deemed a full year and if holding year is more than 10 years, it shall be reduced up to 10 years)

· Deduct/minus the appraised value with the deduction which is fixed at 50% on the appraised value.

· After minus the appraised value with the deduction as mentioned above you will find a result, then divide such result by the holding year, after division you will have YEARLY INCOME.

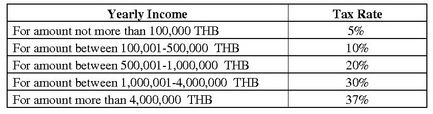

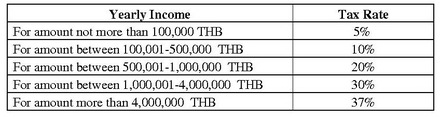

· Calculate YEARLY INCOME TAX by using YEARLY INCOME in accordance with the tax table as follows:

· Finding the appraised value of the property to be sold/transferred.

· Finding the holding year of the property (How long the seller has owned ownership of property counted from the year of receipt of ownership until the year of transfer, any fraction of a year shall be deemed a full year and if holding year is more than 10 years, it shall be reduced up to 10 years)

· Deduct/minus the appraised value with the deduction which is fixed at 50% on the appraised value.

· After minus the appraised value with the deduction as mentioned above you will find a result, then divide such result by the holding year, after division you will have YEARLY INCOME.

· Calculate YEARLY INCOME TAX by using YEARLY INCOME in accordance with the tax table as follows:

· After follow with above stage, you will have the YEARLY INCOME TAX, finally, the PERSONAL WITHHOLDING INCOME TAX shall be the amount of the YEARLY INCOME TAX multiply by HOLDING YEAR (YEARLY INCOME TAX times HOLDING YEAR is PERSONAL WITHHOLDING INCOME TAX)

SAMPLE CALCULATION FOR 3.2

· For example, the appraised value of the property is 4,000,000 THB

· At the transfer date, the seller has owned the property for 4 years and 2 months, so the holding year is 5 years.

· Minus the appraised value (4,000,000 THB) with the deduction (50% of 4,000,000 THB) = 4,000,000 – 2,000,000 = 2,000,000 THB.

· The result from above is 2,000,000 THB, then divide 2,000,000 by 5 (Holding Year), after the division, we have the YEARLY INCOME of 400,000 THB.

· Calculate YEARLY INCOME TAX by using YEARLY INCOME of 400,000 THB in accordance with the below tax table:

· At the transfer date, the seller has owned the property for 4 years and 2 months, so the holding year is 5 years.

· Minus the appraised value (4,000,000 THB) with the deduction (50% of 4,000,000 THB) = 4,000,000 – 2,000,000 = 2,000,000 THB.

· The result from above is 2,000,000 THB, then divide 2,000,000 by 5 (Holding Year), after the division, we have the YEARLY INCOME of 400,000 THB.

· Calculate YEARLY INCOME TAX by using YEARLY INCOME of 400,000 THB in accordance with the below tax table:

For the amount of 100,000 THB, yearly income tax is charged at rate of 5% or 5,000 THB.

For the amount of 300,000 THB, yearly income tax is charged at rate of 10% or 30,000 THB.

The total yearly income tax for yearly income of 400,000 THB is 5,000 + 30,000 = 35,000 THB

· As the final stage, the PERSONAL WITHHOLDING INCOME TAX shall be amount of 35,000 THB multiply by 5 (35,000 x 5 = 175,000 THB

· The personal withholding tax for the sample transaction is 175,000 THB

For the amount of 300,000 THB, yearly income tax is charged at rate of 10% or 30,000 THB.

The total yearly income tax for yearly income of 400,000 THB is 5,000 + 30,000 = 35,000 THB

· As the final stage, the PERSONAL WITHHOLDING INCOME TAX shall be amount of 35,000 THB multiply by 5 (35,000 x 5 = 175,000 THB

· The personal withholding tax for the sample transaction is 175,000 THB

3.3 Calculation of Personal Income Withholding Tax for inherited property and for property acquired by gift, in which located in other area than those referred in 3.2.

The tax can be calculated by stages as follows:

· Finding the appraised value of the property to be sold/transferred.

· Finding the holding year of the property (How long the seller has owned ownership of property counted from the year of receipt of ownership until the year of transfer, any fraction of a year shall be deemed a full year and if holding year is more than 10 years, it shall be reduced up to 10 years)

· Deduct/minus the appraised value with the tax relief amount which is fixed at 200,000 THB.

· Deduct/minus the above result again with the deduction which is fixed at 50% on the above result.

· After minus the result with the deduction as mentioned above you will find another result, then divide such result by the holding year, after division you will have YEARLY INCOME.

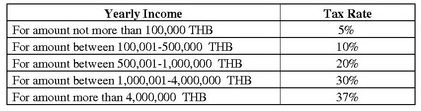

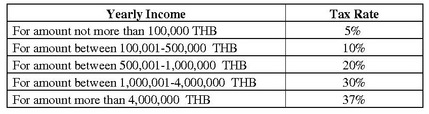

· Calculate YEARLY INCOME TAX by using YEARLY INCOME in accordance with the tax table as follows:

· Finding the appraised value of the property to be sold/transferred.

· Finding the holding year of the property (How long the seller has owned ownership of property counted from the year of receipt of ownership until the year of transfer, any fraction of a year shall be deemed a full year and if holding year is more than 10 years, it shall be reduced up to 10 years)

· Deduct/minus the appraised value with the tax relief amount which is fixed at 200,000 THB.

· Deduct/minus the above result again with the deduction which is fixed at 50% on the above result.

· After minus the result with the deduction as mentioned above you will find another result, then divide such result by the holding year, after division you will have YEARLY INCOME.

· Calculate YEARLY INCOME TAX by using YEARLY INCOME in accordance with the tax table as follows:

· After follow with above stage, you will have the YEARLY INCOME TAX, finally, the PERSONAL WITHHOLDING INCOME TAX shall be the amount of the YEARLY INCOME TAX multiply by HOLDING YEAR (YEARLY INCOME TAX times HOLDING YEAR is PERSONAL WITHHOLDING INCOME TAX)

SAMPLE CALCULATION FOR 3.3

· For example, the appraised value of the property is 4,000,000 THB

· At the transfer date, the seller has owned the property for 4 years and 2 months, so the holding year is 5 years.

· Minus the appraised value (4,000,000 THB) with the tax relief amount which is fixed at 200,000 THB = 4,000,000 – 200,000 = 3,800,000 THB.

· The result from above is 3,800,000 THB, then minus this amount again with the deduction (50% of 3,800,000) = 3,800,000 – 1,900,000 = 1,900,000 THB.

· The result from above is 1,900,000 THB, then divide 1,900,000 by 5 (Holding Year), after the division, we have the YEARLY INCOME of 380,000 THB.

· Calculate YEARLY INCOME TAX by using YEARLY INCOME of 380,000 THB in accordance with the below tax table:

· At the transfer date, the seller has owned the property for 4 years and 2 months, so the holding year is 5 years.

· Minus the appraised value (4,000,000 THB) with the tax relief amount which is fixed at 200,000 THB = 4,000,000 – 200,000 = 3,800,000 THB.

· The result from above is 3,800,000 THB, then minus this amount again with the deduction (50% of 3,800,000) = 3,800,000 – 1,900,000 = 1,900,000 THB.

· The result from above is 1,900,000 THB, then divide 1,900,000 by 5 (Holding Year), after the division, we have the YEARLY INCOME of 380,000 THB.

· Calculate YEARLY INCOME TAX by using YEARLY INCOME of 380,000 THB in accordance with the below tax table:

For the amount of 100,000 THB, yearly income tax is charged at rate of 5% or 5,000 THB.

For the amount of 280,000 THB, yearly income tax is charged at rate of 10% or 28,000 THB.

The total yearly income tax for yearly income of 380,000 THB is 5,000 + 28,000 = 33,000 THB

· As the final stage, the PERSONAL WITHHOLDING INCOME TAX shall be amount of 33,000 THB multiply by 5 (33,000 x 5 = 165,000 THB

· The personal withholding tax for the sample transaction is 165,000 THB

For the amount of 280,000 THB, yearly income tax is charged at rate of 10% or 28,000 THB.

The total yearly income tax for yearly income of 380,000 THB is 5,000 + 28,000 = 33,000 THB

· As the final stage, the PERSONAL WITHHOLDING INCOME TAX shall be amount of 33,000 THB multiply by 5 (33,000 x 5 = 165,000 THB

· The personal withholding tax for the sample transaction is 165,000 THB

Disclaimer: We endeavor to ensure that the information we provide on this website is accurate. However, we do not assume the liability in relation to the accuracy of the information or contents provided, and the information provided should not be construed as legal advice by any means. Should you have more questions or any comment, please contact: [email protected]